Introduction

Understanding the mortgage constant is crucial for first-time homebuyers venturing into the real estate market.

What is a Mortgage Constant?

The mortgage constant is a key financial metric that represents the annual debt service of a mortgage loan as a percentage of the total loan amount. This figure helps homebuyers comprehend their monthly payments and overall financial commitment.

Importance for First-Time Homebuyers

For those entering the housing market, grasping this concept can mean the difference between financial strain and informed decision-making. Knowledge of the mortgage constant empowers buyers to evaluate different loan options, ensuring they choose what best aligns with their budget and long-term goals.

How Hello:Here Can Assist

Navigating the complexities of mortgages can be overwhelming. Hello:Here simplifies this process through its AI-driven property search tools. Our platform provides insights into mortgage constants, enabling first-time homebuyers to understand their financing options better. With Hello:Here, you can approach homebuying with confidence, fully equipped with essential knowledge to make informed choices.

In addition to understanding mortgage constants, it’s also important for potential buyers to consider alternative financing options like seller carry back financing, where the seller acts as the lender. This creative approach can provide more flexibility in financing your property purchase.

Moreover, gaining insights into market trends through methods such as sentiment analysis can significantly benefit buyers by helping them make more informed decisions based on current market sentiments.

Finally, if you’re considering investment properties, understanding rental rates through tools like a multifamily rent survey could greatly enhance your investment strategy.

Understanding Mortgage Constant

The mortgage constant is a crucial figure in real estate finance, reflecting the relationship between a loan amount and its annual payment. This metric simplifies complex mortgage calculations, making it accessible for first-time homebuyers.

What is a Mortgage Constant?

The mortgage constant, often denoted as “k,” represents the annual debt service per dollar of loan. It is calculated as follows:

[ k = \frac{P}{L} ]

Where:

- ( P ) = Annual payment

- ( L ) = Loan amount

Components of Mortgage Constant

- Loan Constant:

- This term refers to the fixed portion of the mortgage that remains constant throughout the life of the loan. It encompasses both principal and interest payments.

- For example, if you take out a loan of $100,000 with an annual payment of $10,000, your loan constant would be 0.1 or 10%.

- Mortgage Capitalization Rate:

- Often used in investment analysis, this rate indicates the expected return on an investment property. It is calculated by dividing net operating income (NOI) by property value.

- A higher capitalization rate typically signals greater risk but also higher potential returns.

Both components work together to provide insight into mortgage costs and investment viability. Understanding these terms enables first-time homebuyers to make informed decisions.

Key Takeaways

- The mortgage constant serves as a vital tool in evaluating loans.

- Recognizing the loan constant and capitalization rate helps demystify financial commitments.

- By mastering these concepts, I empower myself to navigate my home-buying journey effectively.

Understanding your mortgage constant unlocks insights into your financial responsibilities and strengthens your position as a savvy homebuyer.

Moreover, it’s important to recognize how external factors like the economic base can impact real estate investments. This economic foundation drives financial stability and growth in a region.

Additionally, if you’re considering investing in properties with multiple units, understanding multifamily housing and the Build-To-Rent (BTR) concept could be beneficial.

In project management for real estate development, familiarizing yourself with methodologies like the Waterfall model can streamline processes.

If you’re looking into real estate syndications as an investment strategy, knowing about SEC Form D will aid in understanding private securities offerings.

Lastly, grasping concepts such as Gain to Lease, which refers to the difference between actual rent charged and potential market rent, can provide valuable insights for property owners.

Calculating the Mortgage Constant

Understanding how to calculate the mortgage constant is crucial for first-time homebuyers. It provides insights into your monthly debt service obligations and helps you make informed financial decisions. Let’s break down the mortgage constant formula step-by-step.

Mortgage Constant Formula

The mortgage constant (MC) formula is:

[ MC = \frac{Annual Debt Service}{Loan Amount} ]

Where:

- Annual Debt Service is the total amount paid annually, including principal and interest.

- Loan Amount is the total amount borrowed.

Step-by-Step Calculation Example

Consider a hypothetical scenario where you take out a $1,000,000 loan at an annual interest rate of 6%. To find the mortgage constant, follow these steps:

- Calculate Monthly Payment:

- Use the loan payment formula:

- [ M = P \times \frac{r(1 + r)^n}{(1 + r)^n – 1} ]

- Where:

- ( M ) = Monthly payment

- ( P ) = Loan amount ($1,000,000)

- ( r ) = Monthly interest rate (annual rate / 12 months = 0.06 / 12 = 0.005)

- ( n ) = Total number of payments (loan term in months; e.g., 30 years = 360 months)

- Calculate Annual Debt Service:

- Multiply monthly payment by 12 to get annual payment.

- Plug Values into Mortgage Constant Formula:

- Divide the annual debt service by the loan amount.

Example Calculation

For a $1,000,000 loan at 6% over 30 years:

- Monthly payment (M): Approximately $5,995

- Annual debt service: ( $5,995 \times 12 \approx $71,940 )

- Mortgage constant calculation:

[ MC = \frac{71,940}{1,000,000} \approx 0.07194 ]

This means your mortgage constant is about 0.0719, indicating that approximately 7.19% of your loan amount will be paid each year as debt service.

Calculating your mortgage constant empowers you with knowledge about your financial commitment and aids in budgeting effectively. Understanding this metric positions you to manage your mortgage more confidently as you embark on homeownership.

Factors Influencing Mortgage Constant Values

Understanding the factors that influence mortgage constant values is crucial for first-time homebuyers. These elements play a significant role in determining your monthly payments and overall loan cost.

Key Influencing Factors:

1. Interest Rates

The most significant factor impacting the mortgage constant. Higher interest rates lead to a larger mortgage constant, increasing your monthly payment. Conversely, lower rates decrease it, making homeownership more affordable.

2. Loan Type

- Fixed-Rate Mortgages: These loans maintain the same interest rate throughout their term. This stability results in a consistent mortgage constant, allowing for predictable budgeting.

- Variable-Rate Loans: Interest rates can fluctuate over time. This variability means mortgage constants may change, potentially leading to higher payments if market rates rise.

3. Loan Term

The length of the loan affects the mortgage constant. Shorter terms generally result in higher monthly payments but lower total interest costs over time. Longer terms spread payments out, resulting in a lower monthly obligation but increased overall interest paid.

Impact on Homebuyers:

Understanding these factors allows you to make informed decisions when choosing a loan type or negotiating terms with lenders. It empowers you to evaluate offers more effectively and choose options that align with your financial goals and risk tolerance.

Grasping how each element influences your mortgage constant sets you up for success in navigating the complexities of home financing.

The Importance of Mortgage Constant in Real Estate Investment Analysis

Understanding the mortgage constant is crucial for real estate investment analysis. It is an essential tool for assessing the financial viability of property investments.

Managing Debt Servicing

For real estate investors, managing debt servicing is critical. The mortgage constant directly affects the investor’s ability to make monthly loan payments. A higher mortgage constant means higher monthly obligations, while a lower constant provides more flexibility in managing cash flow.

Assessing Cash Flow Needs

Investors often evaluate their cash flow needs using the Debt Coverage Ratio (DCR). DCR measures a property’s ability to generate enough income to cover its debt obligations. It is calculated using:

- Net Operating Income (NOI): This represents total revenue from the property minus operating expenses.

- Mortgage Payments: The total monthly payments based on the mortgage constant.

Using these metrics, investors can determine whether a property will provide sufficient returns relative to its financing costs.

Practical Application for Investors

Consider an investor evaluating a rental property with an NOI of $120,000 and annual mortgage payments of $80,000. To find the DCR:

- Calculate DCR = NOI / Mortgage Payments

- DCR = $120,000 / $80,000 = 1.5

A DCR above 1 indicates that the property generates enough income to comfortably cover its debt obligations.

Real estate agents also play a crucial role in this analysis. They can use their expertise to help investors understand how mortgage constants impact investment decisions and outcomes. By providing insights into local market conditions and potential income streams, agents enable informed choices that align with an investor’s financial goals.

However, it’s not just about understanding the numbers. Investors must also be aware of factors like functional obsolescence, which refers to a decrease in property desirability due to outdated features or designs. Additionally, comprehending concepts such as indemnity in real estate transactions can provide legal protection during property dealings.

Moreover, with changes brought by standards like IFRS 16, which transforms how leases are recorded in financial statements, it becomes essential for investors to adapt their strategies accordingly.

Ultimately, understanding the significance of the mortgage constant empowers investors to navigate complex financial landscapes effectively, ensuring sustainable growth and profitability in their portfolios.

Benefits of Understanding Your Mortgage Constant as a First-Time Homebuyer

Understanding your mortgage constant offers several crucial advantages for first-time homebuyers. This knowledge directly impacts financial decision-making and long-term investment strategies.

1. Enhanced Financial Clarity

Grasping the mortgage constant equips you with a clear understanding of your monthly payment obligations relative to the loan amount. This transparency fosters better budgeting and financial planning, enabling you to allocate resources more effectively.

2. Informed Investment Decisions

Comprehending how the mortgage constant influences your property’s cash flow empowers you to make informed choices. A lower mortgage constant often signals a more manageable monthly payment, improving your overall investment profitability assessment over time. For instance, if you’re considering investing in multifamily real estate, understanding the benefits of submetering can further enhance your investment strategy.

3. Negotiation Power

With a solid grasp of the mortgage constant, you can confidently negotiate terms with lenders. Armed with knowledge about how different rates and terms affect your payments, you gain leverage in securing favorable financing options.

4. Risk Assessment

Understanding the components of the mortgage constant allows you to evaluate risks associated with varying interest rates. You can measure potential impacts on cash flow, helping mitigate negative consequences during economic fluctuations.

5. Long-Term Planning

Knowing your mortgage constant aids in projecting future financial scenarios. Whether planning for home improvements or considering resale value, this insight supports strategic long-term thinking. Moreover, understanding the Multiple Nuclei Model of cities, which suggests that urban areas develop around multiple centers or nuclei, can provide valuable context when evaluating the location and potential appreciation of your property.

Embracing this knowledge not only prepares you for homeownership but also sets the stage for making sound investment decisions that align with your financial goals.

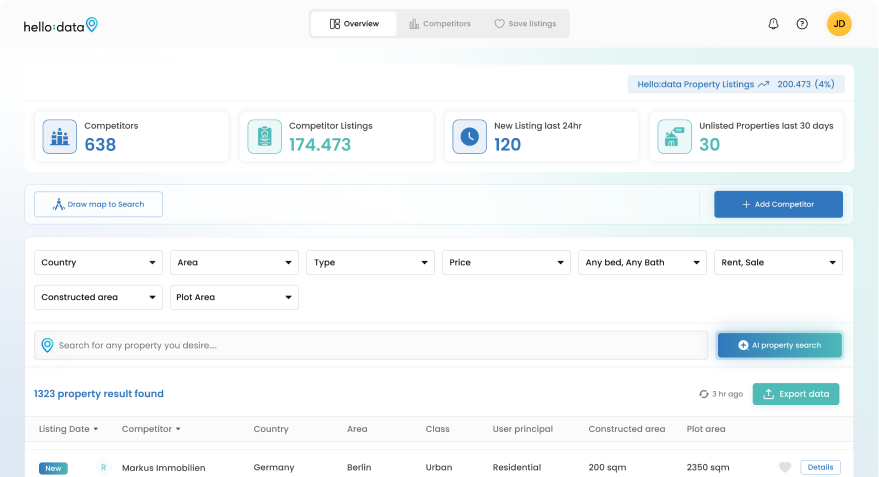

How Hello:Here Simplifies the Mortgage Process for First-Time Homebuyers

Navigating the mortgage landscape can feel overwhelming, especially for first-time homebuyers. Hello:Here is here to empower you with cutting-edge technology and resources that streamline this journey.

1. AI Property Search Feature

Our innovative AI Property Search feature is designed to provide personalized property recommendations tailored to your unique preferences and budget. This technology analyzes your criteria, such as desired location, price range, and property type, to match you with listings that fit your needs. This means no more endless scrolling through irrelevant properties. Instead, focus on what truly matters to you.

2. Real Estate App Functionality

Communication is key in real estate transactions. With Hello:Here, seamless communication with agents becomes a reality. The app allows you to connect directly with real estate professionals who are ready to assist you.

Key functionalities include:

- Instant Messaging: Ask questions and receive answers in real-time.

- Market Data Access: Stay informed with relevant market trends and data at your fingertips.

- Document Sharing: Easily share important documents with agents for faster processing.

Understanding the details of your mortgage is crucial, including concepts like what a mortgage constant is and how it’s calculated. Hello:Here simplifies this process by providing clear explanations within the app. You can easily access resources that break down complex topics into digestible information.

Equipped with these tools, you’re not just another buyer in the market; you’re an empowered participant armed with knowledge and support. Experience the difference as you navigate the mortgage process with confidence and clarity using Hello:Here’s intuitive features designed for first-time homebuyers.

Common Mistakes to Avoid When Dealing with Mortgage Constants as a First-Time Homebuyer

Understanding mortgage constants can be complex. First-time homebuyers often fall into common traps that lead to financial pitfalls. Recognizing these errors is essential for making informed decisions.

Frequent Errors:

- Miscalculating the Mortgage Constant: A simple arithmetic mistake can result in a significant difference in your monthly payments. Double-checking calculations ensures accuracy.

- Ignoring Loan Terms: Not considering how loan terms affect the mortgage constant can skew your understanding of affordability. Different loan durations can alter your payment structure.

- Overlooking the Importance of Interest Rates: Failing to account for fluctuations in interest rates can lead to incorrect assumptions about future payments. Always stay updated on current rates and trends.

- Confusing Loan Constant and Capitalization Rate: These two components, while related, serve different purposes. Understanding each distinctly is crucial for accurate financial planning.

- Neglecting Additional Costs: Mortgage constants typically focus on principal and interest but neglect other costs such as property taxes, insurance, and maintenance fees. These elements significantly impact overall affordability.

- Relying Solely on Online Calculators: While convenient, online tools may not consider personal circumstances or unique loan features. Engaging with a mortgage professional provides tailored insights.

The Impact of Mistakes

Errors made during calculation or interpretation can lead to unexpected financial burdens. Awareness of these pitfalls empowers first-time homebuyers to navigate the mortgage landscape more effectively, ensuring a smoother journey toward homeownership.

In addition to avoiding these common mistakes, first-time homebuyers should also consider leveraging AI-driven market segmentation strategies in their home search. This innovative approach allows buyers to better understand the real estate market by dividing it into subsets of consumers who have common needs, preferences, or characteristics. By understanding these segments, buyers can make more informed decisions and potentially find better deals tailored to their specific requirements.

Conclusion: Empowering First-Time Homebuyers Through Knowledge and Technology

Understanding mortgage constants is crucial for first-time homebuyers. This knowledge not only clarifies what a mortgage constant is but also how it is calculated, enabling informed decision-making in real estate investments.

With the right tools, navigating the complexities of home financing becomes manageable.

- Leverage Knowledge: Grasping mortgage constants equips you with insights into your potential loan repayments and investment viability.

- Innovative Tools: Utilizing platforms like Hello:Here, which is at the forefront of the PropTech revolution, can streamline your search for properties. This innovative AI property search technology makes it easier to match with ideal homes based on your financial landscape.

The integration of technology in real estate empowers buyers to make smarter choices. By combining an understanding of mortgage constants with innovative solutions like those offered by PropTech companies, you can approach your home-buying journey with confidence.

Take charge of your future—use the insights you’ve gained and the tools available to you to navigate the real estate market successfully. With this powerful combination, you’re set to make choices that align with your goals and financial health.