What is a Lockout Period in a Commercial Mortgage?

A lockout period in a commercial mortgage refers to a specified time frame during which the borrower cannot make early repayments on their loan without incurring penalties. This period is established by lenders as part of the loan agreement and serves several important functions.

Key aspects of a lockout period include:

- Protection for Lenders: It ensures that lenders receive expected interest payments over an agreed timeline, minimizing their risk.

- Borrower Considerations: While this might limit flexibility for borrowers, understanding the implications is crucial for financial planning.

Typically, lockout periods can last anywhere from one to five years, depending on the lender and specific loan terms. During this time, borrowers are often restricted from refinancing or paying off their loan early.

Understanding what a lockout period in a commercial mortgage entails is vital for both parties involved. It sets clear expectations and helps in strategizing financial decisions effectively.

For instance, if you are considering investing in multifamily real estate, understanding what a good cap rate is could be beneficial. This metric represents the relationship between a property’s net operating income (NOI) and its purchase price.

Furthermore, the advent of Artificial Intelligence in Real Estate is revolutionizing the property market, transforming every aspect of the buying, selling, and management process.

Moreover, understanding what a PropTech company is can provide insights into how innovative technology is reshaping the real estate industry.

As an example of this transformation, consider Hello:Here’s AI property search system, which is making property search and management easier through advanced artificial intelligence features.

Lastly, it’s important for real estate investors to grasp concepts such as breakeven occupancy, which represents the minimum occupancy level required for a property to cover its operating expenses and debt service without incurring losses.

Understanding Lockout Periods

A lockout period in a commercial mortgage is a specific timeframe during which the borrower is prohibited from paying off the loan before its maturity date without incurring penalties. This mechanism serves as a safeguard for lenders, ensuring they recoup their investment and maintain interest income over the life of the loan.

Detailed Definition of a Lockout Period

In simpler terms, when we ask what is a lockout period, it refers to the designated time during which borrowers are locked into their mortgage agreements. This means that any attempt to pay off the principal amount early—whether through refinancing or selling the property—could trigger significant penalties. The exact terms and conditions surrounding this lockout will be outlined in the loan agreement.

Purpose and Significance in Commercial Mortgages

The purpose of implementing a lockout period is multifaceted:

- Risk Mitigation for Lenders: By locking borrowers into their loans, lenders can effectively reduce the risk associated with fluctuating interest rates. Should interest rates rise, lenders benefit from higher returns on their fixed-rate loans.

- Financial Stability: Lockout periods encourage financial stability within the lending environment. They help ensure that lenders have consistent cash flow for a predetermined duration.

- Long-Term Planning: For both parties, having clarity on payment obligations fosters long-term planning. Borrowers can manage their finances more predictably, while lenders can forecast revenue streams accurately.

Understanding this significance helps clarify why these periods are common in commercial mortgages. They create balance within financial transactions, benefiting both lenders and borrowers in the long run.

Typical Duration of Lockout Periods

Lockout periods vary widely depending on lender policies and market conditions. Generally, they can last anywhere from one to five years, although some loans may have shorter or longer durations. Factors influencing this duration include:

- Type of Property: Investment properties may face longer lockouts due to perceived risks.

- Loan Amount: Larger loans often come with extended lockout periods as lenders seek to secure their investments.

- Market Conditions: In times of economic uncertainty, lenders may impose longer lockouts to hedge against potential borrower defaults.

Borrowers should always review these terms carefully and consider how they align with their financial strategies. It’s crucial to understand the implications of a lockout period in commercial mortgage agreements before committing to any contract, ensuring that you are prepared for any constraints it may impose on your financial flexibility moving forward.

In such situations, understanding how rental rates work can be crucial for property owners and investors who want to make informed decisions. This is where a multifamily rent survey comes in handy.

Moreover, technological advancements like ClickPay, which simplifies the complicated process of collecting rent and managing finances, are also changing the landscape of real estate transactions significantly.

As we move further into 2024, it’s important to note how AI technology is revolutionizing rental listings and making them more efficient.

The Role of Lenders and Borrowers

Lockout periods in commercial mortgages serve as a critical mechanism that protects lenders’ interests while presenting unique challenges for borrowers. Understanding this dynamic is essential for navigating the complexities of financing.

Benefits for Lenders

Lenders gain several advantages from implementing lockout periods:

- Risk Mitigation: A lockout period ensures that the lender has a guaranteed return on investment during the initial years of the loan. This stability allows lenders to manage their risk more effectively, especially in volatile markets.

- Interest Rate Security: During the lockout phase, lenders can count on consistent interest payments without the worry of early loan payoffs. This predictability aids in financial planning and resource allocation.

- Preservation of Loan Structure: Lockout periods prevent borrowers from refinancing immediately, which could disrupt the lender’s financial projections. Lenders prefer to keep loans intact until they are fully amortized or until significant equity is built.

- Strengthened Relationships: By enforcing lockout periods, lenders can cultivate long-term relationships with borrowers. This extended commitment can lead to further business opportunities down the line.

Risks and Considerations for Borrowers

Borrowers face distinct risks and considerations during lockout periods:

- Limited Flexibility: The inability to repay or refinance loans during the lockout limits a borrower’s options, particularly if market conditions shift or if their financial situation changes unexpectedly.

- Potential Financial Strain: If interest rates decrease or property values rise significantly, borrowers may feel trapped paying higher rates than what might be available in the market. This disparity can create financial pressure as businesses seek to maximize earnings.

- Opportunity Costs: The time spent under a lockout period may prevent borrowers from capitalizing on more favorable financing arrangements that could arise. By being locked into their current terms, they may miss out on advantageous investment opportunities.

- Penalties for Early Repayment: If a borrower wishes to exit their loan early despite a lockout period, they may incur hefty penalties. Understanding these penalties is crucial before entering into any mortgage agreement.

Navigating these intricacies requires careful consideration of both lender benefits and borrower risks. By being informed about how lockout periods function within commercial mortgages, borrowers can make empowered decisions that align with their financial strategies and future goals.

Moreover, leveraging technology such as SFR analytics tools can provide valuable insights into real estate trends and help in making informed decisions during such challenging times. Additionally, understanding models like the Waterfall model in project management could also assist in structuring projects effectively amidst these financial constraints.

Financial Implications of Lockout Periods

Lockout periods significantly shape the financial landscape for borrowers in commercial mortgages. Understanding these implications is crucial for effective financial planning and strategy.

Impact on Borrowers’ Financial Strategies

- Cash Flow Management: During a lockout period, borrowers are restricted from paying off their loans early. This can lead to a more predictable cash flow management strategy since borrowers must account for fixed interest payments over the duration of the lockout.

- Interest Payments: Interest payments accumulate during the lockout, which may affect the overall cost of borrowing. Borrowers should consider how long they will be locked into paying interest without the option to pay down principal.

- Future Financing Plans: A lockout period may hinder opportunities for refinancing or acquiring new financing options. Borrowers must strategize around these limitations, often requiring more foresight in their financial planning.

Prepayment Penalties

Early repayment during a lockout period typically incurs penalties. Understanding these potential penalties is essential:

- Types of Penalties:

- Flat Fee Penalties: A predetermined fee that applies if a borrower pays off the mortgage early.

- Percentage-Based Penalties: A percentage of the remaining loan balance due at the time of early payoff.

- Calculating Costs: For example, if a borrower has a $1 million mortgage with a 5% prepayment penalty and decides to pay it off during the lockout, they could face an additional cost of $50,000. This emphasizes the importance of assessing potential penalties against anticipated savings from early repayment.

Strategic Considerations

Borrowers should adopt proactive measures to navigate these financial implications:

- Long-Term Projections: Assessing long-term interest rates and economic trends can help in making informed decisions about whether to commit to a lockout period. Understanding the role of economic base in real estate investments can also provide valuable insights into market conditions.

- Negotiation Leverage: Engaging with lenders about flexible terms can provide valuable negotiating power. Discussing variable options or lower penalties can lead to more favorable terms.

- Alternative Financing Solutions: Exploring other financing mechanisms outside traditional mortgages might mitigate some risks posed by lockout periods. Leveraging advanced technologies such as AI property search can also streamline property acquisition processes.

Understanding how lockout periods influence your financial strategy is vital. Recognizing potential penalties associated with early repayment creates an avenue for smarter planning and better decision-making throughout your mortgage journey. With this knowledge, you can position yourself for success despite the constraints imposed by a lockout period in your commercial mortgage.

Impact on Refinancing Options

Lockout periods impose specific limitations on refinancing options for borrowers. Understanding these restrictions can help you navigate the complexities of commercial mortgages effectively.

Limitations Imposed by Lockout Periods

- Restricted Access to Funds: During a lockout period, borrowers cannot pay off their loan early or refinance without facing significant penalties. This restriction limits your ability to access capital that could be used for other investments or opportunities.

- Market Changes: If interest rates decrease during your lockout period, you are unable to take advantage of refinancing at a lower rate. This situation can lead to missed opportunities for cost savings over the loan’s life.

- Equity Growth: Changes in property value may also affect your refinancing potential. If property values appreciate, being locked into a higher-rate mortgage can hinder your ability to capitalize on increased equity.

- Debt-to-Income Ratio: A lockout period can restrict your financial flexibility, impacting your debt-to-income ratio when seeking additional financing options.

Strategies for Borrowers to Manage Refinancing Post-Lockout

Planning ahead can mitigate some of the challenges posed by a lockout period. Here are effective strategies:

- Monitor Interest Rates: Keep an eye on market trends and interest rates during the lockout period. This awareness enables you to act swiftly once the lockout ends.

- Evaluate Loan Terms Early: Review your current loan terms well before the end of the lockout period. Identify any potential prepayment penalties and understand how they may impact future refinancing options.

- Build Relationships with Lenders: Establishing rapport with lenders can facilitate smoother negotiations when you’re ready to refinance post-lockout. A strong relationship may result in better terms or more flexible options.

- Prepare Your Financial Profile: Strengthen your credit score and ensure all financial documents are in order prior to the end of the lockout period. A solid financial profile increases your attractiveness as a borrower, potentially leading to favorable refinancing conditions.

- Consider Alternative Financing Options: Explore other forms of financing that may not be subject to traditional lockout restrictions, such as lines of credit or second mortgages. These alternatives could provide needed liquidity while waiting for the lockout period to expire.

Understanding the impact of lockout periods on refinancing is crucial for making informed decisions regarding commercial mortgages. By implementing these strategies, you position yourself for success and adaptability once you have the freedom to refinance your loan.

Moreover, if you’re considering leveraging property value through platforms like Airbnb, it’s worth noting that Airbnb Plus offers a unique alternative that might provide additional financial flexibility during such periods.

Types of Prepayment Penalties

When a commercial mortgage lockout period ends, several types of prepayment penalties may apply. Understanding these penalties is crucial for borrowers aiming to manage their financial obligations effectively. Here’s a breakdown of the key prepayment restrictions:

1. Step-Down Lockout Penalties

This type of penalty decreases over time, typically in relation to the mortgage term. For example, if a loan has a step-down penalty structure, the penalty might be 5% if paid off in the first year after the lockout, reducing to 3% in the second year and possibly 1% in the third year.

Borrowers benefit from lower penalties as they approach the end of their mortgage term. This structure incentivizes long-term commitment while providing flexibility as time progresses.

2. Yield Maintenance Penalties

Yield maintenance is designed to ensure that lenders receive a specific yield on their investment, regardless of when the loan is paid off. The penalty calculates the present value of future cash flows lost due to early repayment.

It factors in current interest rates compared to the original loan rate. If market rates decrease, borrowers may face significant penalties as lenders seek compensation for lost interest income.

This type of penalty can be complex and costly for borrowers who decide to refinance or pay off their loans early.

Comparison Between Step-Down and Yield Maintenance Penalties

|

Feature Step-Down Lockout Penalty Yield Maintenance Penalty Penalty Structure |

Decreases over time |

Fixed based on future cash flows |

|

Incentive for Borrowers |

Encourages longer commitments |

Protects lender’s expected yields |

|

Complexity |

Straightforward |

Complex calculations required |

|

Financial Impact |

Predictable reduction in penalties |

Potentially high costs if rates drop |

Understanding these prepayment penalties empowers borrowers to make informed decisions about refinancing or selling property after a lockout period. Awareness of potential costs and benefits associated with each type ensures that your financial strategy aligns with your business objectives.

As you consider your options post-lockout, being proactive about evaluating these penalties will help you navigate your financial landscape effectively. Knowing how each penalty operates aids in planning for potential scenarios and making strategic moves that align with your long-term goals. Recognizing these nuances places you in a stronger position when negotiating loan terms or refinancing options in the future.

Negotiating Loan Terms

When it comes to securing a commercial mortgage, negotiating loan terms is crucial. Engaging in an open dialogue with lenders can significantly impact your financial strategy, particularly regarding lockout periods.

Importance of Discussing Lockout Terms

Understanding the implications of a lockout period is essential for both current and future financial planning. Discussing these terms with lenders before signing agreements can help uncover potential pitfalls and opportunities. Key points to consider include:

- Clarity on Duration: Ensure you know how long the lockout period lasts. This timeframe affects when you can make adjustments to your mortgage without penalties.

- Prepayment Penalties: Inquire about any associated penalties for early repayment during and after the lockout period. Knowing these details allows for better budgeting and financial forecasting.

- Flexibility Options: Ask about possible options for flexibility within the lockout period. Some lenders may offer limited exceptions or modifications that could be beneficial in unforeseen circumstances.

Being proactive in these discussions not only enhances transparency but also empowers you to make informed decisions that align with your business objectives.

Alternatives for Borrowers Seeking Flexibility

If the standard lockout terms seem restrictive, exploring alternative loan options might be advantageous. Consider the following alternatives:

- Adjustable-rate Mortgages (ARMs): These loans often provide lower initial rates, which can be beneficial if you’re willing to manage potential fluctuations in payments over time.

- Shorter Lockout Periods: Negotiate for a shorter lockout duration if possible. This flexibility could allow you to refinance or sell sooner without incurring hefty penalties.

- Exit Strategy Plans: Discuss exit strategies that allow you to adjust your loan terms based on market conditions or business needs. This approach provides a safety net during uncertain economic times.

- Hybrid Loans: Some lenders offer hybrid loans combining fixed and variable rates, providing both stability and flexibility. Investigate whether this option aligns with your financial goals.

Engaging with lenders about these alternatives reinforces your commitment to finding the best financial solutions tailored to your needs. Increased awareness of all available options allows you to navigate complex scenarios more confidently.

Negotiating loan terms isn’t merely about securing funds; it’s about crafting a partnership that supports long-term success. As you evaluate different strategies, keep in mind how each choice aligns with your overall vision for growth within the commercial real estate landscape.

Incorporating strategies like submetering into your property management approach can further enhance your investment’s profitability, making it an essential aspect of your overall financial strategy.

Hello Here: Revolutionizing Real Estate Financing with AI

In a rapidly evolving real estate landscape, Hello Here SL emerges as a game-changing platform that uses artificial intelligence (AI) to transform how we approach commercial mortgages. Understanding complex terms like lockout periods becomes seamless with innovative technology.

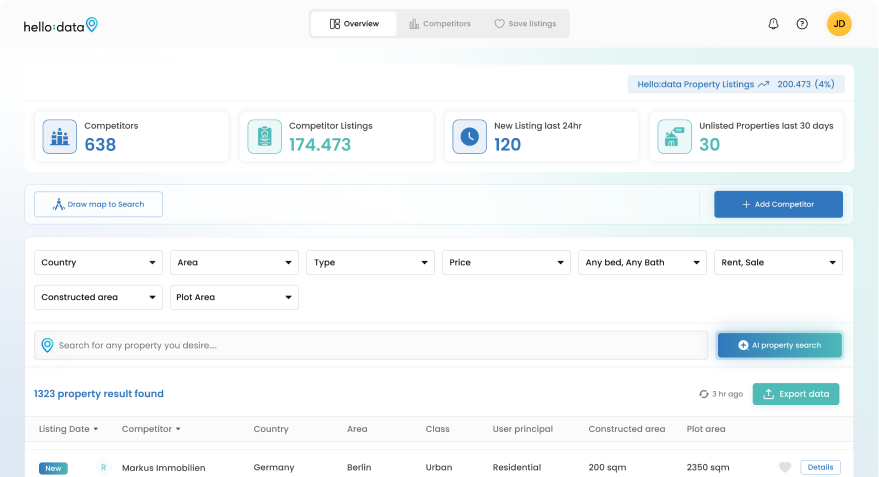

Enhancing Property Search Efficiency with Hello Data’s Capabilities

Hello Data, a core component of the Hello Here ecosystem, revolutionizes property search through advanced data aggregation and analysis. Here’s how it empowers borrowers:

- Comprehensive Listings: With more listings than traditional platforms, Hello Data offers an extensive database—over 82,000 properties in Mallorca alone. This capability ensures you have access to a broader range of options when considering investments.

- Data Analysis Tools: The platform provides sophisticated analytical tools that help users evaluate properties effectively. By comparing market trends and pricing data, borrowers can make informed decisions regarding mortgages impacted by lockout periods.

- User-Friendly Experience: The intuitive design makes navigating through various listings easy, similar to using a dating app. This approach minimizes the overwhelming nature of property searches and allows for targeted results based on user preferences.

Borrowers can leverage these features to gain insights into potential investments while being mindful of terms like lockout periods. Accessing real-time data enables strategic planning around financing options and prepayment penalties.

Addressing the Lockout Challenge

Navigating lockout periods in a commercial mortgage can be daunting. Hello Here simplifies this process by providing clarity on how these terms could affect your financial strategies. Using AI-driven insights allows borrowers to:

- Understand Financial Implications: Knowing the duration of lockout periods helps in forecasting cash flow and budgeting for future expenses.

- Explore Refinancing Options: Post-lockout strategies become clearer through detailed analyses of property values and market conditions.

Empowering Decision-Making

With Hello Here, making informed decisions about real estate investments becomes attainable:

- Real-Time Updates: Stay ahead with notifications about market changes or new listings that fit your criteria.

- Tailored Recommendations: The AI property matching app suggests properties that align with your investment goals while considering the nuances of financing options.

- Educational Resources: Access valuable information regarding common mortgage terms, including lockouts, ensuring you are well-equipped during negotiations.

Incorporating technology into real estate financing changes how borrowers interact with lenders. By leveraging innovations from platforms like Hello Here SL, individuals can take charge of their financial futures while navigating complex mortgage terms effectively.

Seller Carry Back Financing: A Smart Move for Real Estate Investors

One innovative approach that has emerged in the realm of real estate financing is the seller carry back option. This creative financing method allows buyers to purchase properties directly from sellers who act as lenders, often leading to more favorable terms for both parties involved.

The integration of AI into real estate financing is not just about efficiency but also about empowerment. Borrowers gain access to crucial information needed to navigate the complexities associated with commercial mortgages. Understanding what a lockout period means becomes less intimidating when you have the right tools at your disposal.

With companies like Hello Here, the future of real estate financing looks brighter. Whether you’re searching for investment opportunities or looking to streamline your mortgage process, embracing technology will lead to