Introduction

The Secured Overnight Financing Rate (SOFR) is a benchmark interest rate that reflects the cost of borrowing cash overnight, secured by U.S. Treasury securities. It has become an important part of real estate financing.

Why SOFR Matters in Real Estate

Here are some key reasons why SOFR is significant:

- Transparency: SOFR is based on actual transactions, making it a more reliable indicator than previous benchmarks like LIBOR.

- Lower Borrowing Costs: With SOFR, borrowers often enjoy reduced rates compared to traditional options, translating into significant savings over time.

SOFR is fundamentally changing how real estate transactions are financed. This change not only makes loans more affordable but also creates a fairer lending environment. By using advanced technology and working with platforms that offer Proptech and Artificial Intelligence, SOFR makes processes easier for both lenders and borrowers.

The Impact of SOFR on the Market

As we see the positive effects on market dynamics, expectations are high. Understanding what SOFR means in real estate is crucial for anyone involved in property transactions today. Embracing this new benchmark will help you make informed financial decisions and take advantage of opportunities in a changing market.

Additional Factors Influencing Real Estate Investments

There are several other factors that can impact real estate investments:

- Regulation D: The integration of Regulation D into real estate investments adds complexity and opportunity. This set of rules established by the Securities and Exchange Commission (SEC) allows companies to raise capital without extensive registration.

- Sentiment Analysis: Understanding market dynamics can be enhanced through sentiment analysis, which provides insights by analyzing various sources such as social media and news articles.

- Accounting Standards: It’s important to stay updated on accounting standards like IFRS 16, which changes how leases are recorded in financial statements and impacts leasing practices in the real estate sector.

These factors, combined with the influence of SOFR, shape the landscape of real estate investments and require stakeholders to adapt their strategies accordingly.

Understanding SOFR

The Secured Overnight Financing Rate (SOFR) has become an important benchmark in the financial world, especially for real estate deals. By understanding how it’s calculated and its significance, we can better appreciate its potential effects.

How SOFR Is Calculated

SOFR is based on transactions in the U.S. Treasury repurchase market, where banks and other financial institutions borrow and lend money using U.S. Treasury securities as collateral. Here’s how it works:

- Data Collection: SOFR relies on actual transaction data, which includes billions of dollars in overnight financing activity.

- Weighted Average: The rate is calculated as a volume-weighted average of the rates paid on these transactions, ensuring accuracy and reliability.

This robust methodology contributes to SOFR’s credibility, distinguishing it from alternative benchmarks.

Comparison Between SOFR and LIBOR

The transition from LIBOR (London Interbank Offered Rate) to SOFR represents a significant change in how interest rates are determined for various financial products, including mortgages. Here are the key differences:

- Transaction Basis: While LIBOR was based on estimated rates at which banks believed they could borrow from one another, SOFR relies on actual market transactions. This fundamental change makes SOFR less susceptible to manipulation.

- Market Representation: LIBOR included multiple tenors (different maturities), whereas SOFR is purely an overnight rate. This focus provides clarity but can also impact long-term borrowing strategies.

Advantages of Using SOFR

Using SOFR as a benchmark offers several benefits:

- Increased Transparency: The reliance on observable market data enhances transparency, fostering trust among borrowers and lenders.

- Lower Borrowing Costs: As lenders adopt this reliable benchmark, competition increases, potentially lowering borrowing costs for consumers.

- Stability and Predictability: With a movement towards a more stable foundation for interest rates, borrowers can expect fewer fluctuations compared to LIBOR-linked products.

SOFR’s introduction indicates not only an evolution in financial benchmarks but also a commitment to fairer lending practices in real estate financing. The move towards a more robust and transparent system signals progress in the industry.

In project management, particularly in software development, understanding the implications of such financial shifts is crucial. For instance, adopting the Waterfall model in project management requires a solid grasp of financial metrics like SOFR that could influence budget allocations and resource management.

Impact on Adjustable-Rate Mortgages (ARMs)

The transition to SOFR is reshaping the landscape of adjustable-rate mortgages (ARMs). This shift introduces several key changes in ARM structures and pricing mechanisms.

1. New Pricing Mechanisms

SOFR provides a more stable benchmark than LIBOR, leading to a recalibration of how ARM interest rates are set. This adjustment can create more predictable payment schedules for borrowers, reducing uncertainty associated with rate fluctuations.

2. Advantageous Initial Rates

Borrowers opting for ARMs linked to SOFR may benefit from lower initial rates. The competitive nature of SOFR-driven products could lead lenders to offer attractive starting rates, making homeownership more accessible.

3. Greater Stability Over Time

With SOFR’s emphasis on actual transactions in the U.S. Treasury repurchase market, borrowers can experience enhanced stability in their mortgage payments. This reliability diminishes the volatility traditionally associated with ARMs tied to LIBOR.

The potential for refinancing also becomes a consideration. As borrowers evaluate their options, those linked to SOFR might find it easier to transition to more favorable terms if interest rates change significantly.

The integration of SOFR into adjustable-rate mortgages signifies a positive shift for borrowers, fostering an environment where cost-effectiveness and stability are prioritized. Embracing these changes positions me for smarter financial decisions and a clearer understanding of future mortgage obligations.

Influence on Commercial Real Estate Loans

The transition to SOFR (Secured Overnight Financing Rate) is reshaping the landscape of commercial real estate financing. As a benchmark, SOFR offers numerous advantages for commercial loans, enhancing both pricing competitiveness and risk management capabilities.

Key Benefits:

- Improved Loan Pricing Competitiveness: SOFR’s reliance on actual transactions in the U.S. Treasury repurchase market means it reflects current market conditions more accurately than previous benchmarks like LIBOR. This leads to more favorable loan terms and potentially lower borrowing costs for businesses.

- Enhanced Risk Management: By using a transparent benchmark, lenders can better assess the risks associated with their loan portfolios. The predictability of SOFR promotes informed decision-making, allowing lenders to craft more tailored financing solutions that meet diverse borrower needs.

- Attractiveness for Borrowers: The shift to SOFR empowers borrowers by providing clearer insights into their financing costs. As businesses look to expand or invest in property, understanding how SOFR impacts commercial loans allows them to make strategic financial decisions.

What is SOFR in Real Estate?

SOFR represents a significant evolution in how commercial real estate loans are structured. Its adoption not only streamlines the lending process but also aligns interest rates with broader economic trends, ultimately benefiting both lenders and borrowers.

With these advancements in mind, commercial real estate stakeholders are poised to leverage the benefits of SOFR as they navigate financing options in an ever-evolving market.

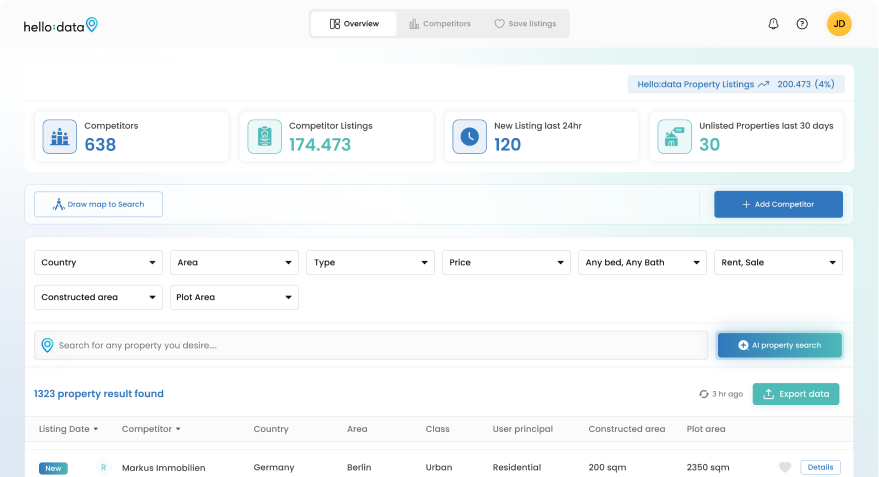

Moreover, the integration of AI technology into the real estate sector is revolutionizing property management and search processes. Platforms like Hello:Here, which utilize AI property search features, are setting new industry standards by making property search and management easier.

Furthermore, understanding metrics such as breakeven occupancy can significantly influence investment decisions. For a comprehensive guide on this crucial metric, refer to this detailed article on breakeven occupancy.

In addition to these insights, leveraging tools like SFR analytics can provide precise and actionable data essential for making informed investment decisions.

Changes in Mortgage Rates Due to SOFR Adoption

The widespread adoption of SOFR is set to reshape the landscape of mortgage rates, bringing significant implications for both borrowers and lenders. Key factors include:

- Lower Borrowing Costs: As SOFR becomes the benchmark, competition among lenders may increase, leading to more favorable rates for borrowers. This could translate into lower monthly payments and reduced overall costs.

- Stability in Interest Rates: The transition from LIBOR to SOFR is expected to introduce a level of stability often missing in previous benchmarks. With a transparent and reliable rate, borrowers can enjoy predictability in their financial planning.

- Long-Term Benefits: Over time, the impact on mortgage rates may lead to a more favorable borrowing environment. Lenders adopting SOFR can better manage risks, which could foster an ecosystem that encourages lending at lower interest rates.

As we look to the future, the dynamics between fixed-rate mortgages and adjustable-rate mortgages (ARMs) will change:

- Fixed-Rate Mortgages: Traditionally seen as a safe choice, fixed-rate mortgages may become less attractive compared to ARMs linked to SOFR.

- Adjustable-Rate Mortgages (ARMs): Borrowers opting for SOFR-linked ARMs might benefit from lower initial rates. These loans can offer an appealing alternative as they adjust less frequently and are tied to a benchmark with greater market relevance.

In this evolving landscape, understanding the nuances of mortgage rates will empower borrowers to make informed decisions that align with their financial goals. For example, if you’re considering investing in property as a long-term strategy, you might want to explore options like AirBNB Plus or delve into how a multifamily rent survey could boost your investment.

Advantages of Embracing a Transparent Benchmark Like SOFR

The introduction of the Secured Overnight Financing Rate (SOFR) marks a crucial moment in real estate financing. A reliable and transparent benchmark interest rate like SOFR is essential for several reasons:

1. Fairer Lending Practices

Transparency in lending is crucial. SOFR’s reliance on actual transactions from the U.S. Treasury repurchase market ensures that it reflects true market conditions. This reduces the potential for manipulation, creating a level playing field for borrowers and lenders alike.

2. Predictability in Rates

With SOFR, borrowers gain clarity about how their interest rates are calculated. Unlike LIBOR, which faced scrutiny over its reliability, SOFR is based on observable data. This provides a more stable foundation for pricing loans, offering borrowers enhanced predictability when managing their finances.

3. Enhanced Risk Management

Lenders benefit from improved risk assessment capabilities. A transparent benchmark allows them to better evaluate loan performance and adjust strategies accordingly. This leads to more responsible lending practices, ultimately benefiting the entire real estate ecosystem.

4. Consumer Confidence

Trust in the lending process increases with transparent benchmarks. When borrowers understand how rates are determined, they feel more empowered in their decisions, fostering a healthier marketplace where informed choices prevail.

Adopting SOFR not only supports fairer lending but also strengthens the entire financial landscape in real estate. As we embrace this new standard, we set the stage for a more equitable and efficient future in property transactions.

Moreover, the integration of technology, particularly AI, into the real estate sector is transforming various aspects such as rental listings. This technological revolution complements the advantages offered by adopting SOFR, thereby enhancing overall efficiency and transparency in the real estate market.

Challenges Faced During The Transition Phase Towards A More Stable Future With SOFR-based Products And Services In The Market

Transitioning to SOFR presents unique challenges for the real estate industry. Understanding these concerns is vital for a successful shift.

Key Concerns from Lenders

- Adoption Rates: Many lenders worry about how quickly borrowers will embrace SOFR-based products. Transitioning from established benchmarks like LIBOR can create uncertainty.

- Inaccuracies in Early Stages: Initial implementation may lead to discrepancies in pricing and risk assessment. This can affect both lenders and borrowers, creating potential pitfalls during the transition.

Strategies to Mitigate Risks

- Education and Awareness: Providing comprehensive resources on what SOFR is in real estate helps demystify the new benchmark. Workshops, webinars, and informational materials can equip all stakeholders with necessary knowledge.

- Gradual Implementation: Phasing in SOFR-based products allows time for adaptation. Starting with a pilot program can help identify issues before a full rollout.

- Enhanced Communication: Maintaining open dialogues between lenders and borrowers fosters trust. Regular updates on market conditions and product offerings can ease anxieties around adoption.

- Collaboration with Financial Institutions: Partnerships among lenders can lead to shared insights, promoting best practices and improved standards across the industry.

By addressing these challenges head-on, the real estate sector can pave the way for a more stable future with SOFR at its core, ensuring a smoother transition that benefits everyone involved.

How Hello Here is Changing the Way People Buy and Sell Property

Hello Here is changing the real estate game with its AI property search app. This innovative platform connects buyers and sellers, customizing property matches based on personal preferences and financing options like SOFR. Here’s how Hello Here helps users in this new world:

Finding the Perfect Property with AI

The app uses advanced algorithms, including Support Vector Machines, to analyze user inputs, ensuring the most relevant properties are presented. This personalized approach enhances the property search experience, making it more efficient and enjoyable.

Understanding Financing Costs Made Easy

Real estate financing can be complicated. Hello Here makes it simple with instantaneous cost calculators, allowing users to quickly assess potential mortgage payments and other financial obligations.

Customized Loan Recommendations for Every User

Hello Here understands that each user’s financial situation is different. That’s why it offers tailored recommendations for suitable loan products and service providers. This feature aligns financing options with individual needs, making it easier for users to make informed decisions.

Learning About SOFR’s Impact on Real Estate

In addition to finding properties, Hello Here provides valuable insights into how SOFR affects real estate transactions. Users gain a clearer understanding of how this benchmark impacts their borrowing costs and overall purchasing power.

These features not only make the property search process smoother but also give buyers and sellers important knowledge in a rapidly changing market. By using AI technology and prioritizing user-friendly design, Hello Here aims to lead the way in the future of real estate financing.

As we move forward, reliable benchmarks like SOFR being integrated into platforms such as Hello Here will make real estate transactions more transparent and efficient. This shift marks a new era where technology meets finance, ultimately benefiting everyone involved.

Moreover, understanding concepts such as As Stabilized Value in real estate investments or using geospatial analysis to boost home sales can further improve decision-making for buyers and sellers alike. Additionally, employing tools like Comparative Market Analysis will help investors determine property values more accurately.

Future Trends In Real Estate Financing Driven By Advancements In Technology Like AI Alongside The Continued Evolution Of Benchmarks Such As SOFR Over Time

The world of real estate financing is about to change. The use of SOFR as a standard is just the start. With technology improving, especially with AI, we will see big changes in how real estate deals are done.

Predictions for the Future

- Streamlined Processes: Expect a gradual departure from traditional methods. Digital platforms will rise, using advanced algorithms to facilitate transactions.

- Real-Time Insights: Integration with reliable data sources like Treasury markets enables access to real-time pricing dynamics. This fosters informed decision-making for buyers and sellers alike.

Innovations on the Horizon

The shift towards efficiency will bring forth several innovations:

- Smart Contracts:

- Automated execution phases will eliminate the need for intermediaries.

- Buyers and sellers can engage directly through secure channels, enhancing communication efficiency.

- Reduced reliance on third-party institutions minimizes delays and cuts costs.

- Enhanced Data Utilization:

- AI-driven insights will offer tailored strategies based on individual market conditions.

- Access to comprehensive property data enables better forecasting and investment planning.

- Personalized Financing Solutions:

- Platforms will leverage user data to suggest financing products that align with unique financial situations.

- Dynamic interest rate adjustments based on market fluctuations will empower borrowers to choose optimal loan options.

- Integration of Blockchain Technology:

- Transactions could utilize blockchain for transparent records, ensuring security and trustworthiness.

- This technology facilitates seamless transfers of assets, reducing risks associated with fraud.

- Increased Market Accessibility:

- Advanced real estate platforms will democratize access to market information.

- Smaller investors gain opportunities typically reserved for larger entities, cultivating a more diverse investment landscape.

Economic Perspective

From an economic standpoint, these trends signify a shift towards greater efficiency in real estate financing:

- Traditional systems often introduce friction points that slow down transactions.

- A digital-first approach enhances speed and responsiveness in processing deals.

As we embrace these technological advancements alongside the evolution of benchmarks like SOFR, the future of real estate financing looks promising. The combination of AI, smart contracts, and transparent benchmarks has the potential to transform how business is conducted in this industry, making it more accessible and efficient than ever before.

Moreover, staying updated on real estate news is crucial for making informed decisions as the market evolves rapidly due to economic shifts, policy changes, and emerging technologies.

Understanding concepts such as opportunity zones, which are designated areas where investors can receive significant tax incentives for investing in economically distressed regions, can also provide valuable insights into potential investment opportunities.

In addition to these advancements, it’s important to comprehend terms like ingress and egress which significantly impact property accessibility and value.

Furthermore, with the rise of AI in real estate, AI property search is becoming increasingly popular as it allows users to find rental properties that match their specific preferences and requirements efficiently.

Conclusion

The impact of SOFR on the real estate market is profound. This transition to a more stable benchmark holds promise for various stakeholders:

- Homebuyers: Access to affordable financing options empowers individuals to make informed purchasing decisions, enhancing their ability to secure homes in desirable locations.

- Investors: Institutional investors can benefit from well-structured portfolios. Diverse asset classifications, including residential and commercial properties, remain attractive even amid economic uncertainties.

Key points to consider:

- Transparency: SOFR promotes clearer pricing mechanisms, reducing ambiguity in loan structures. This transparency fosters trust between lenders and borrowers.

- Long-Term Stability: The shift towards SOFR signifies a commitment to long-term stability in financial markets, providing confidence for strategic investments.

Understanding what SOFR is in real estate is crucial as its adoption represents a pivotal moment in how transactions are financed. This transition not only benefits individual buyers but also plays a significant role in shaping the broader liquidity in real estate, allowing properties to be bought or sold quickly without significantly impacting their price.

Moreover, it provides insights into the role of economic base in real estate investments, which refers to the economic foundation of a region driving its financial stability and growth.

Additionally, understanding sectors like multifamily housing and Build-To-Rent (BTR) can further enhance investment strategies. Embracing these changes positions all stakeholders for success as we move forward into an evolving economic environment.