Introduction

The forward LIBOR curve is a crucial concept in real estate financing. It represents future interest rates derived from current market data, helping investors anticipate borrowing costs.

Significance in Real Estate Financing

- Impacts variable-rate loans and adjustable-rate mortgages (ARMs)

- Affects overall investment strategies and decision-making

Understanding the forward LIBOR curve is essential for real estate investors. It directly influences how you approach financing options, ultimately shaping your investment outcomes.

Hello:Here, a leading Proptech company, offers tools and insights to help navigate the complexities of the forward LIBOR curve. Their expertise can empower you to make informed financial decisions, simplifying your path to success in real estate.

In addition to understanding the forward LIBOR curve, leveraging advanced technologies like geospatial analysis can significantly enhance your real estate strategies. This approach has proven beneficial in various regions, including Spain, where it has been used to maximize home sales.

Moreover, understanding valuation models such as the automated valuation model or conducting a thorough comparative market analysis can further refine your investment strategies. These tools and insights are invaluable for navigating the complexities of real estate financing and investment.

Understanding the Forward LIBOR Curve

The forward LIBOR curve represents future interest rates anticipated for borrowing over specific periods. It serves as a critical benchmark for financial products, influencing decisions in real estate financing.

Definition and Role

The forward LIBOR curve is derived from the London Interbank Offered Rate (LIBOR), a global reference rate reflecting the cost of borrowing between banks. This curve helps to establish expectations for future interest rates and is instrumental in pricing various financial instruments, including:

- Forward Rate Agreements (FRA): Contracts that lock in an interest rate for a future period.

- Interest Rate Swaps (IRS): Agreements to exchange fixed interest payments for floating ones based on LIBOR.

Historical Context of LIBOR

Since its introduction, LIBOR has been a cornerstone of global finance. Its significance in real estate financing is particularly evident through:

- Adjustable-Rate Mortgages (ARMs): Loans where interest rates fluctuate, often tied to LIBOR. Borrowers benefit when rates are low but face risks if they rise.

- Commercial Loans: Many commercial real estate loans utilize LIBOR to set variable interest rates, affecting borrowers’ cash flow and overall investment strategies.

The transition away from LIBOR due to regulatory changes underscores its importance in understanding risk management in real estate financing. Keeping abreast of these developments is essential for making informed investment choices.

In this context, understanding effective rents becomes crucial as they directly influence the cash flow of properties financed through ARMs or commercial loans tied to LIBOR rates. Additionally, it’s important to consider models such as the waterfall model in project management, which can provide valuable insights into managing real estate projects effectively amidst fluctuating interest rates.

Furthermore, with the increasing emphasis on sustainability in real estate, understanding concepts like sustainable occupancy could be beneficial. This knowledge can help investors make more informed decisions about property investments, especially in a market where LIBOR’s influence is gradually diminishing.

The Mechanics Behind the Forward LIBOR Curve

Understanding how forward LIBOR rates are estimated offers valuable insights into real estate financing. The essence lies in discount factors, which play a crucial role in determining future cash flows associated with variable-rate loans.

Forward Rate Estimation

Forward rates are derived from the relationship between spot rates and their corresponding discount factors. The formula used is as follows:

[ F(t) = \frac{(1 + S(t+n))^n}{(1 + S(t))^t} – 1 ]

Where:

- F(t) represents the forward rate for a period starting at time t.

- S(t) denotes the spot rate at time t.

- n indicates the length of time until the forward rate takes effect.

This formula highlights how current interest rates influence expectations about future borrowing costs, making it essential for real estate investors to grasp these mechanics.

Multi-Curve vs. Mono-Curve Frameworks

The landscape of interest rate derivatives is shaped by two primary frameworks: multi-curve and mono-curve.

Mono-Curve Framework

- Utilizes a single yield curve for all types of interest rate products.

- Simplifies pricing but may lead to inaccuracies when assessing different financial products.

Multi-Curve Framework

- Employs distinct curves for various instruments, such as swaps and bonds.

- Provides a more precise pricing mechanism by accounting for differing liquidity and risk profiles among instruments.

The choice between these frameworks significantly impacts how interest rate derivatives are priced, influencing borrowing strategies in real estate financing. Understanding these mechanics equips investors with the tools to navigate complex financial landscapes effectively.

Impact of Interest Rates on Real Estate Financing Decisions

The forward LIBOR curve plays a crucial role in shaping real estate financing, especially for variable-rate loans. Understanding its implications allows borrowers to make informed decisions about their financing strategies.

Influence on Variable-Rate Loans

Variable-rate loans are directly tied to the forward LIBOR curve. An increase in future LIBOR rates suggests higher borrowing costs, impacting cash flow projections and overall investment returns. Borrowers must consider:

- Interest Rate Derivatives: Instruments like caplets and floors can be utilized to hedge against rising rates. A caplet protects borrowers by capping interest payments, while a floor guarantees a minimum return on investments.

- Risk Management Strategies: Implementing strategies such as interest rate swaps can help stabilize cash flows amidst fluctuating rates.

Fixed-Rate vs. Variable-Rate Options

When evaluating financing options, both fixed and variable rates present unique advantages and drawbacks:

- Fixed-Rate LoansPros: Provide certainty in payment amounts; shield borrowers from future interest rate hikes.

- Cons: Often come with higher initial rates compared to variable options; limit flexibility if market rates decrease.

- Variable-Rate LoansPros: Typically feature lower starting rates; potential for reduced payments as the market stabilizes or declines.

- Cons: Payments can increase significantly if the forward LIBOR curve predicts rising interest rates; exposure to market volatility.

Strategic Considerations

Investors should analyze the forward LIBOR curve’s predictions carefully when choosing between fixed and variable-rate options. The decision hinges on individual risk tolerance and financial objectives. With accurate forecasting from the forward curve, investors can navigate potential pitfalls and seize favorable opportunities in an evolving market landscape.

In addition to understanding interest rate impacts, staying updated with the latest trends is crucial. For instance, knowing the best sources of real estate news in 2024 can provide valuable insights into market dynamics.

Furthermore, comprehending aspects like liquidity in real estate, or understanding terms such as ingress and egress can enhance one’s investment strategy.

Additionally, being aware of concepts like opportunity zones or replacement reserves in real estate can further empower investors in making informed decisions.

Lessons Learned from Financial Crises: Their Influence on Interest Rate Curves

The financial crisis of 2007-2008 served as a pivotal moment in the evolution of interest rate understanding. This disruption offered critical insights into how market volatility can affect interest rate determination and valuation. Here are key lessons drawn from this period:

1. Market Reactions

The crisis resulted in drastic shifts in investor sentiment, leading to heightened risk aversion. This behavior directly influenced the forward LIBOR curve, causing it to reflect uncertain future conditions.

2. Correlation Impact on FRA Valuation

Forward Rate Agreements (FRAs) became essential tools for hedging against interest rate volatility. The correlation between forward rates and actual market movements highlighted the need for robust risk management strategies.

3. Changes in Benchmarking Practices

Post-crisis, the integrity of LIBOR came under scrutiny, prompting regulators to seek more reliable benchmarks. This led to discussions around transitioning to alternatives such as SOFR, altering investors’ approaches to financing.

4. Risk Exposure Awareness

As the crisis unfolded, many realized their exposure to variable-rate loans. Understanding how changes in the forward LIBOR curve could impact borrowing costs became crucial for long-term planning.

These insights underscore the importance of learning from past financial disruptions. By analyzing historical events, real estate investors can better navigate interest rate curves and make informed financing decisions moving forward. Recognizing these patterns enhances our ability to anticipate future shifts in the market landscape.

Practical Applications of the Forward LIBOR Curve in Real Estate Investment Valuation and Cash Flow Projections

Understanding how to value properties with variable-rate financing is critical for real estate investors. The forward LIBOR curve provides a framework for assessing future interest rate movements, which directly impacts investment decisions. Here’s how it works:

1. Valuation of Forward Rate Agreement Adjustments

In a multi-curve framework, forward rates are derived from current market yields. This allows investors to adjust their property valuations based on anticipated changes in interest rates, enabling more informed decision-making. For example, if the forward curve predicts rising rates, an investor may need to recalibrate cash flow expectations and property value assessments accordingly.

2. Cash Flow Projections

Accurate cash flow forecasting is essential for property investments influenced by interest rates. Using the forward LIBOR curve, investors can project future cash flows by incorporating expected rate changes into their financial models. This approach helps in evaluating the long-term viability and profitability of an investment.

Investors should pay close attention to:

- Inflation Terms: Consider inflation expectations when using the forward curve for projections. Rising inflation can affect both nominal interest rates and real returns, making cash flow analysis even more complex.

- Sensitivity Analysis: Conduct sensitivity analyses to understand how different scenarios could affect property valuations under varying interest rate environments.

- Investment Strategies: Develop strategies that leverage insights from the forward curve, such as locking in favorable rates or opting for hedging options to mitigate risks associated with rising rates.

Moreover, leveraging advanced technologies like AI can significantly enhance these processes. For instance, AI has revolutionized property search methods, making it easier for investors to find suitable properties that align with their financial projections and valuation models. With systems like HelloHere’s AI property search, investors can streamline their property search process while gaining valuable insights into potential investments.

Additionally, understanding the role of economic base in real estate investments is crucial for making informed decisions. By utilizing the forward LIBOR curve effectively alongside these advanced tools and insights, investors can enhance investment valuation accuracy and support robust cash flow projections, ultimately leading to better-informed business strategies in real estate investing.

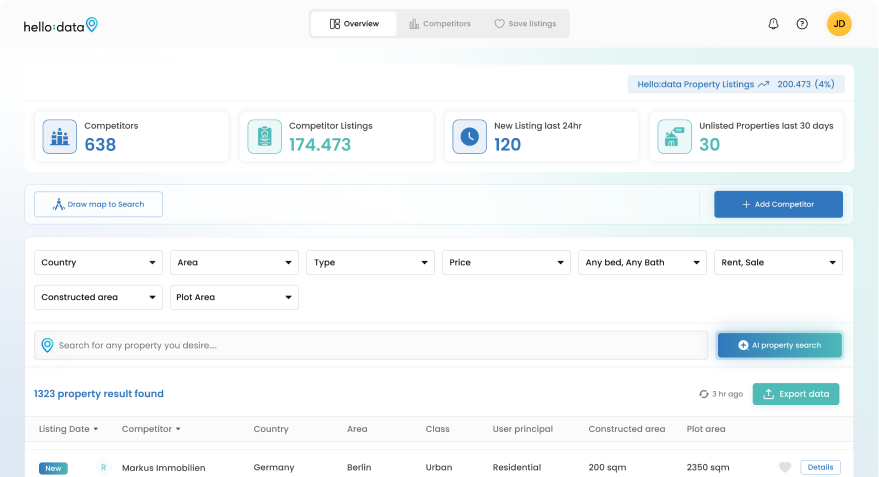

The Role of AI in Enhancing Property Search: A Case Study with Hello:Here

Hello:Here is changing the way people search for properties by using AI technology on its platform. This is especially important for investors who are trying to understand the complexities of real estate financing, particularly when it comes to the forward LIBOR curve.

How AI Improves Property Search

1. Market Trend Analysis

Hello:Here uses AI algorithms to study changes in interest rates and property values. This ability helps investors make informed decisions based on data rather than guessing. For example, how market segmentation is changing real estate with AI can give investors valuable information about specific market trends.

2. Better Property Matching

By understanding what users like and using large amounts of data, Hello:Here makes property matching more effective. Investors get personalized listings that match their specific investment requirements, increasing their chances of finding the perfect opportunities. This AI property search tool greatly enhances the property search experience for both buyers and renters.

3. Continuous Adjustments

The AI constantly learns from market trends. As interest rates fluctuate, so do the recommendations given to users. This ensures that investors are always aware of how changes in the forward LIBOR curve may affect their financing options and potential profits.

Benefits for Investors

Investors gain a lot from this approach driven by AI:

- More precise property searches

- Improved ability to predict cash flows influenced by interest rate movements

- More strategic investment decisions based on up-to-date information

With features like a lease rent optimizer, Hello:Here demonstrates how technology can improve traditional practices in real estate. By combining AI with fundamental financial concepts such as the forward LIBOR curve, it empowers investors to seize opportunities and effectively navigate potential risks.

Furthermore, the platform’s capability to find rental units on MLS and ILS broadens its usefulness for prospective renters. Compared to other platforms like YieldStar LRO and AIRM, Hello:Here stands out as a better option in the ultimate AI property search comparison.

Future Directions for Real Estate Financing: Transitioning from LIBOR to Alternatives such as SOFR or Bank of England Rates

The financial landscape is evolving. The transition from LIBOR to alternative benchmarks like SOFR (Secured Overnight Financing Rate) and Bank of England rates signifies a monumental shift in real estate financing.

Key considerations in this transition include:

- Reliability: SOFR, being based on actual transactions in the Treasury repurchase market, offers greater transparency and reliability compared to LIBOR.

- Market Adoption: As financial institutions adapt, the adoption of SOFR is gaining momentum. This shift can lead to more standardized pricing across various financial products.

- Impact on Borrowing Costs: The change in benchmark could influence interest rate dynamics, affecting both fixed-rate and variable-rate loans. Investors must stay attuned to these changes.

Understanding how these new benchmarks will affect loan pricing and risk management strategies is crucial. For instance, utilizing SFR analytics tools can provide valuable insights during this transition. Additionally, comprehending regulation D and its impact on real estate investments is vital for navigating these changes effectively.

Adapting to this transformation ensures that real estate investors remain competitive in a rapidly changing market environment. The future of real estate financing hinges on embracing these alternatives, paving the way for more secure and predictable borrowing practices. As we move forward, understanding how to value real estate will be essential. Furthermore, leveraging tools like regression analysis can significantly enhance our understanding of the market dynamics at play.

Conclusion

Staying informed about the forward LIBOR curve is essential for successful real estate investing strategies. Understanding the impact of the forward LIBOR curve on real estate can significantly influence your borrowing costs and investment decisions.

- Key points to remember:The forward LIBOR curve serves as a crucial benchmark.

- Its fluctuations directly affect variable-rate loans.

- Knowledge of this curve empowers investors to make informed choices.

Explore innovative solutions like Hello:Here that leverage technology and expert insights. With our AI-driven approach, navigating the complexities of interest rate curves becomes more accessible and efficient.

As you embark on your real estate journey, prioritize understanding what the forward LIBOR curve means for your investments. Embrace growth and innovation with tools designed to enhance your decision-making process.