Understanding Loan-to-Value Ratio (LTV) in Real Estate

What is LTV in Real Estate?

The loan-to-value ratio (LTV) is a critical financial metric used in real estate transactions. It measures the amount of a loan compared to the appraised value of the property being purchased. A lower LTV indicates less risk for lenders, while a higher LTV suggests greater risk.

How LTV is Calculated

The LTV ratio is calculated using the following formula:

[ \text{LTV} = \left( \frac{\text{Loan Amount}}{\text{Appraised Property Value}} \right) \times 100 ]

Example:

If you are purchasing a home valued at $300,000 and you put down $60,000 as a down payment, your loan amount would be $240,000. The LTV calculation would look like this:

[ \text{LTV} = \left( \frac{240,000}{300,000} \right) \times 100 = 80% ]

In this example, an LTV of 80% indicates that the buyer is financing 80% of the property’s value.

Significance of LTV in Real Estate Transactions

Understanding loan-to-value ratios is essential for both buyers and lenders. Here’s why:

- Risk Assessment: Lenders use LTV to assess the risk associated with a mortgage. Higher LTV ratios may result in stricter lending criteria.

- Mortgage Terms: An elevated LTV can lead to higher interest rates and additional costs, such as private mortgage insurance (PMI).

- Investment Decisions: For buyers, knowing their LTV helps them understand their equity stake in the property and informs future investment decisions.

Understanding the loan-to-value ratio arms you with knowledge crucial for navigating real estate transactions confidently. Take control of your financial future by grasping these key concepts surrounding LTV.

Moreover, it’s important to consider other factors like the as stabilized value, which refers to the estimated value of a property once it has reached its optimal state. This understanding can further enhance your decision-making process in real estate investments.

In today’s digital age, leveraging advanced technologies such as Support Vector Machines can provide significant advantages in property analysis and valuation. These powerful algorithms are transforming how we approach real estate by providing more accurate data-driven insights.

To stay updated on market trends and make informed decisions, it’s crucial to have access to reliable sources of information. Here are some of the best sources of real estate news in 2024 that can help you stay informed about economic shifts, policy changes, and emerging technologies affecting the market.

Furthermore, utilizing techniques like geospatial analysis can significantly enhance your understanding of property values and trends by analyzing geographical data and mapping techniques.

The Impact of LTV on Mortgage Lending

Understanding the Loan-to-Value (LTV) ratio is crucial for both buyers and lenders. LTV plays a significant role in assessing lending risk, influencing mortgage eligibility criteria. A higher LTV indicates that a borrower is financing a larger portion of the property’s value, which can raise concerns about their ability to repay the loan. Conversely, a lower LTV suggests a stronger financial position, often leading to more favorable terms.

Effects of High and Low LTV Ratios

High LTV Ratios (Above 80%)

- Potentially riskier for lenders

- Often leads to higher interest rates due to perceived increased risk

- Requires Private Mortgage Insurance (PMI), adding to monthly expenses

- May limit options for borrowers seeking favorable terms

Low LTV Ratios (Below 80%)

- Generally viewed as lower risk

- Can secure lower interest rates, benefiting borrowers in the long run

- PMI may not be required, reducing overall costs

- Opens doors to better loan conditions and flexibility

Key Considerations

The impact of LTV on interest rates cannot be overstated. A high LTV ratio increases the likelihood of default from a lender’s perspective, resulting in elevated interest rates. This means that borrowers with higher ratios might pay significantly more over the life of their loans compared to those with lower ratios.

In addition, mortgage insurance requirements create further implications. Borrowers with high LTVs must often purchase PMI to protect lenders against potential losses. This additional cost can strain budgets and affect homeownership affordability.

Understanding these dynamics is essential for anyone entering the real estate market. Awareness of how LTV influences mortgage lending decisions prepares buyers to navigate their options effectively while seeking out favorable loan terms.

Moreover, for investors looking into multifamily properties, understanding rental rates through tools such as a multifamily rent survey can significantly boost investment returns.

As the real estate landscape evolves, leveraging technology becomes increasingly important. This is where PropTech companies come into play, transforming traditional buying and selling processes with innovative solutions.

Furthermore, platforms like Hello:Here are changing the game with their AI property search features, making property search and management easier than ever before.

For those looking to maximize their real estate insights, utilizing SFR analytics tools can provide precise and actionable data crucial for informed investment decisions.

Lastly, real estate investors should also familiarize themselves with key metrics such as breakeven occupancy, which represents the minimum occupancy level required for a property to cover its operating expenses and debt service without incurring losses.

Exploring Different Types of Loans and Their Maximum LTV Ratios

Understanding the types of loans available in the real estate market is essential for making informed decisions. Each loan type has distinct maximum Loan-to-Value (LTV) ratios, which can significantly impact your financing options.

1. Conventional Loans

These are not backed by a government entity and typically have a maximum LTV ratio of 80%. This means borrowers must make at least a 20% down payment. Higher down payments can lead to better interest rates.

2. FHA Loans

Insured by the Federal Housing Administration, FHA loans cater to first-time homebuyers and those with lower credit scores. They allow for a maximum LTV ratio of up to 96.5%, requiring just a 3.5% down payment. This makes them an attractive option for many buyers.

3. USDA Loans

Designed for rural properties, USDA loans offer 100% financing, resulting in a maximum LTV ratio of 100%. No down payment is necessary, which opens doors for eligible buyers looking to invest in rural areas.

Familiarity with these loan types and their respective LTV limits is crucial in navigating the mortgage landscape effectively. Understanding these parameters empowers borrowers to choose the right financing solution tailored to their needs and financial situation.

Moreover, as AI and technology continue to change the landscape, it’s important to stay updated on market trends. Utilizing tools like sentiment analysis can provide valuable insights into buyer preferences and market dynamics.

Additionally, understanding the differences between Airbnb Plus and traditional rentals can also influence your investment decisions, especially in the rental market.

The Relationship Between Down Payment Amounts and LTV Ratios

Understanding how down payments affect loan-to-value (LTV) ratios is crucial for any real estate transaction. The LTV ratio is a key metric that lenders use to assess risk, and it is directly influenced by the size of the down payment.

LTV Calculation

The formula for calculating LTV is straightforward:

[ \text{LTV} = \left( \frac{\text{Loan Amount}}{\text{Property Value}} \right) \times 100 ]

For example, if you are purchasing a property valued at $300,000 and make a down payment of $60,000, the loan amount will be $240,000. The LTV calculation would be:

[ \text{LTV} = \left( \frac{240,000}{300,000} \right) \times 100 = 80% ]

Impact of Down Payment Amount

A higher down payment leads to a lower LTV ratio. This reduction in LTV can result in:

- Better mortgage terms: Lower interest rates

- Reduced mortgage insurance requirements: Potential savings on monthly payments

Conversely, a smaller down payment increases the LTV ratio, which may lead to:

- Higher interest rates

- Mandatory private mortgage insurance (PMI)

Recognizing this relationship empowers buyers to make informed financial decisions when entering the real estate market. Understanding down payment amounts’ impact on loan-to-value ratios plays a vital role in shaping your financing strategy.

In today’s digital age, platforms like Clickpay, designed specifically for the real estate industry, are simplifying the process of making significant financial decisions such as down payments. These innovative solutions not only streamline transactions but also provide valuable insights into managing finances effectively.

Moreover, with advancements in technology such as AI property search, buyers can now find properties that best suit their financial capabilities and personal preferences. This revolution in property search enables potential homeowners to make better-informed decisions regarding their down payments and subsequently their LTV ratios.

Additionally, understanding complex models like the Multiple Nuclei Model of Cities, can provide deeper insights into urban development patterns which can influence property values and ultimately affect your financial strategy in real estate investments.

Managing Risk: The Role of Financial Institutions in Controlling LTV Levels

Financial institutions play a critical role in monitoring loan-to-value (LTV) ratios, as these figures are essential for assessing borrower risk. Here’s how banks approach this vital process:

1. LTV in Risk Assessment

LTV ratios provide insight into the borrower’s equity in the property. A higher LTV indicates less equity, which can signal greater risk to lenders.

2. Regulatory Guidelines

Various regulations guide banks in their lending practices:

- Basel III: International regulatory framework emphasizing capital requirements.

- Consumer Financial Protection Bureau (CFPB): Establishes rules to protect consumers, influencing how banks assess LTV.

3. Risk-Based Pricing

Based on LTV calculations, lenders may adjust interest rates and terms. A higher LTV often results in increased interest rates or additional fees, reflecting the heightened risk taken on by the lender.

4. Portfolio Management

Financial institutions monitor aggregate LTV levels across their loan portfolios to maintain a balanced risk profile. This oversight helps prevent systemic issues that could arise from excessive lending to high-risk borrowers.

Understanding the financial institutions’ role in monitoring loan-to-value ratios equips borrowers with the knowledge needed for making informed decisions about loans and property investments. However, it’s also crucial to understand the role of economic base in real estate investments, as this factor significantly influences property values and investment success. Furthermore, leveraging technology such as AI property search tools can greatly enhance the property search process, making it more efficient and tailored to individual needs.

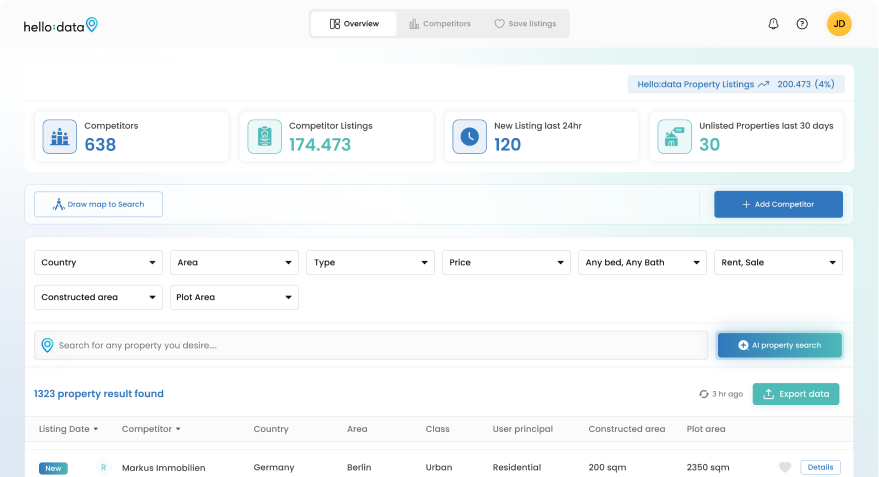

Hello Here: Revolutionizing Property Searches with AI Technology

Discover Hello Here SL, an innovative proptech solution transforming the way we search for properties. In a market flooded with options, finding the right home can feel overwhelming. Hello Here leverages cutting-edge AI technology to streamline property searches, making them faster and more efficient.

Key Features of Hello Here

- AI-Driven Listing Enhancements: The platform utilizes advanced algorithms to curate listings tailored to individual preferences. This personalized approach ensures users find properties that align with their specific needs.

- Improved Property Matching: By analyzing user behavior and preferences, Hello Here provides matches that traditional platforms struggle to achieve. The result? A more intuitive and satisfying home search experience.

Addressing Gaps in Traditional Listings

Traditional property listings often present challenges like outdated information, limited search capabilities, and overwhelming choices. Hello Here addresses these issues by:

- Aggregating Data: With access to over 82k properties in Mallorca alone, Hello Data outperforms competitors like Idealista, which lists only 24k properties.

- Real-Time Updates: Users receive timely updates on available properties, ensuring they have the latest information at their fingertips.

Efficiency through AI Technology

Hello Here’s AI-driven technology significantly boosts property matching efficiency. This innovative approach offers several advantages:

- Speed: Users can quickly sift through countless listings to find their dream home without feeling bogged down.

- Precision: The platform enhances accuracy in matching properties based on user-defined criteria.

- User Empowerment: By harnessing AI, users can take control of their home searches with confidence.

Comparison with Traditional Platforms

Compared to established platforms like Zillow, Hello Here stands out due to its unique features:

- Comprehensive Data Integration: While Zillow may provide a broad range of listings, it often lacks the nuanced understanding of buyer preferences that Hello Here excels at.

- User Experience Focus: The design philosophy behind Hello Here prioritizes user experiences that feel more akin to a dating app than a conventional property search interface.

Benefits for Users

Utilizing Hello Here’s technology means enjoying a seamless property search experience characterized by:

- Tailored Matches: Each listing aligns closely with user preferences.

- Enhanced Decision-Making: With curated options at their disposal, users can make informed decisions confidently.

In addition to these benefits, Hello Here‘s AI-driven property search also revolutionizes the way renters and landlords navigate the real estate market.

Moreover, understanding complex real estate concepts is essential for making informed decisions. For instance, knowing about opportunity zones in real estate can provide significant tax incentives for investors. Similarly, a comparative market analysis is an essential tool that helps real estate investors determine the value of a property.

In a world where real estate transactions are evolving rapidly, embracing tools like Hello Here is essential for anyone looking to navigate the market effectively. By prioritizing innovation and personalization, Hello Here redefines what it means to search